Visa Cross-Border Solutions:

AI-Driven Recipient Choice + Instant Credential Issuance for Cross-Border Platform Payouts

Visa | Hypothetical 2025–2027

Visa Orbit: Recipient Choice Portal

CONTEXT

Late 2025. Only 36% of gig/creator platforms offered truly instant payouts globally (PYMNTS Intelligence 2025). More than 70% of online gig workers reported frustration with slow, expensive, or unavailable cross-border payments (Visa Money Travels Report 2025 + internal surveys).

Platforms repeatedly told us in discovery: “We juggle 6–10 payout providers to cover all corridors. Reconciliation is a nightmare, failure rates hit 8–12% in Africa and LATAM, and angry recipients flood our support.”

Visa Direct already reached 3B+ billion cards and wallets, yet platforms routed <25% of their volume through us because we lacked true recipient-side flexibility and intelligent routing. Leadership’s “new flows” mandate was explicit: win the platform payout layer in 2025–2028 or permanently lose it to Stripe, Payoneer, Deel, Airwallex, and stablecoin-native solutions.

If we give recipients real choice of receive method (bank, wallet, cash pickup, or instant Visa credential) with AI pre-selecting the fastest/cheapest option for them, then payout success rates will exceed 98%, recipient NPS >70, and platforms will shift 40%+ more volume to Visa rails (because happy recipients = happy platforms that consolidate providers)

HYPOTHESIS

THE MARKET

What can we learn from competitors?

The platform payout space (gig, creator, marketplace, seller disbursements) is one of the most fiercely contested segments in all of fintech in 2025, with estimated cross-border volume of $400–550B and growing 18–22% YoY (McKinsey Global Payments 2025, BCG Global Payments 2025).

No one has yet built the clear “default layer,” so consolidation is happening extremely fast — platforms are ruthlessly cutting from 6–10 providers down to 1–3 in order to eliminate reconciliation overhead and reduce failure rates.

Competitive landscape:

Stripe Treasury / Connect → Still the default for e-commerce and newer marketplaces. Excellent developer experience, but FX markups remain high (1–2%+), routing intelligence lags in emerging markets, and they have zero control over recipient-side experience once money leaves their system.

Payoneer → Legacy leader for freelancer platforms (long-time Upwork partner). Very strong coverage, but recipient complaints about withdrawal fees, slow local bank transfers in Tier-2 corridors, and clunky UI persist in 2025.

Deel / Remote → Dominating the EOR + payroll bundle. Deel deepened its Wise + Airwallex stack throughout 2025 and began aggressively pushing its own Deel Card as the receive method. High overall take-rate (2–4% all-in) is causing high-volume platforms to look elsewhere for pure-play payouts.

Airwallex / Thunes / dLocal / Rapyd → The “smart routing” pure-plays. Best-in-class multi-rail engines (local ACH, wallets, instant rails), often achieving <1% all-in cost and 95%+ same-day delivery. Fatal flaw: no owned acceptance network — once the money hits the recipient’s wallet or bank, the provider relationship ends. No credential issuance, no long-term interchange.

Wise Platform → The cost leader for <$10k transfers. Transparent mid-market FX + low fees made it the consolidation winner for many platforms in 2024–2025. Weaknesses remain: batch-only in some corridors, occasional 24–48h delays to certain wallets, no real-time card fallback, and no credential issuance.

Emerging threats → Circle / Coinbase / Stripe Stablecoin payouts – near-zero cost for platforms that will accept USDC, but regulatory friction and recipient crypto-adoption still limit this to <5% of volume outside crypto-native platforms.

Key trend confirmed throughout 2025:

Key trend confirmed throughout 2025: Platforms are executing aggressive provider consolidation programs to reduce ops headcount and failure rates.

Real examples:

Deel publicly moved ~85% of non-EOR payout volume to Wise + Airwallex in H1 2025

OnlyFans completed a payout audit in late 2024 and cut from 9 to 3 core providers in Q1 2025, citing “recipient NPS” as the #1 criteria

Upwork issued an RFP in September 2025 explicitly seeking a single strategic partner that can replace their remaining five rails

Large SEA marketplace (confidential) told us in discovery they will drop from 8 → 2 providers in 2026 if success rate hits 98.5%+

What does this mean for Visa ?

The winner-take-most dynamic is now crystal clear: the provider that delivers the highest recipient satisfaction (choice + speed + inclusion via credential) at >98% success rate will capture the entire flow of the platform — and lock in volume for years through issued credentials.

This is Visa opportunity is enormous: we have the acceptance network and credential issuance capability no one else has. We just need to match (or beat) the routing intelligence and recipient experience of the pure-plays. The Recipient Choice Portal is exactly the wedge to do it.

After evaluating all major cross-border segments (corporate B2B, consumer remittances, travel/e-com, insurance/aid, platform payouts), I chose platform payout operators and their individual recipients as the highest-leverage segment for 2025–2028 because:

Highest growth (15–20%+ CAGR)

Strongest consolidation dynamics (platforms actively want to drop 6–10 providers)

Unique credential issuance opportunity (millions of unbanked/underbanked recipients in emerging markets → lifelong interchange)

Fiercest competitive threat (fintechs aggressively taking share here)

Perfect fit for recipient-choice feature (individuals have strong local preferences; corporates do not)

Who is Visa’s Target user?

THE AUDIENCE

User Insights

Platform payout leads (15 discovery interviews Q3–Q4 2025):

“If a recipient in Nigeria complains three times, they churn. We lose the worker and the client.”

“I would kill for one provider that just lets the recipient pick what works for them. I don’t care about the rail — I care about success rate and not getting yelled at.”

“Reconciliation across 8 providers costs me 3 FTEs. Get me to 2 providers total and I’ll route everything possible through you.”

Recipient surveys (n=1,200 across PH/IN/MX/NG):

82% want choice of receive method

67% prefer digital wallet when available (GCash, M-Pesa, Paytm, etc.)

59% would choose “instant Visa card” if offered (even at slight premium) because spendable immediately

Biggest frustration: “I wait 3–5 days and then still have to go to an agent.”

Primary User

Payout/Finance Ops leads at global digital platforms (gig, creator, marketplace, seller payouts) sending $50M–$2B cross-border annually.

Persona: “Alex the Payout Ops Lead” – 32–45yo, US/EU-based, highly technical, reports to CFO/VP Finance, bonus tied to payout cost reduction + contractor/creator retention, currently manages Airtable + 8 payout partners + weekly reconciliation fires.

Secondary (critical):

Recipients – freelancers, creators, sellers in Philippines, India, Mexico, Nigeria, Indonesia, Pakistan, Egypt, Bangladesh (top 8 receive markets = ~65% of global platform payout volume).

Without explicit usage data around the use cases listed above, I have made inferences about user behaviour based on prevailing market sentiment

To design the most impactful cross border payments features, we’ll solve core pain points for a target user segment based on these primary use cases. To summarize, we’ll be focusing on users who are:

Payout/Finance Ops leads at global digital platforms (gig, creator, marketplace, seller payouts) sending $50M–$2B cross-border annually.

How does our target user’s current user journey look like ?

USER JOURNEY

What are the pain points that these users need addressed?

USER INSIGHTS

1. Fragmented provider stack forces constant manual work

Spends 10–15 hours/week splitting batches in Excel/Airtable by country and method

Maintains 6–10 separate integrations, logins, and pricing agreements

Every new country launch requires 2–4 weeks of testing another provider

4. No control over recipient experience

Recipients stuck with whatever rail Alex chose — often slow or expensive for them

Support tickets spike every payout cycle: “Why is it taking 5 days?” / “Why so many fees?”

Platforms lose top earners to competitors who pay faster (e.g., Deel’s instant wallet)

2. Reconciliation is a weekly nightmare

3–5 FTEs (or expensive outsourcer) just to match settlements across providers

Daily “Missing” or delayed payouts create accounting black holes that hit in audits

FX gains/losses impossible to track accurately → CFO asks Alex why costs are volatile

5. Inability to serve unbanked/underbanked recipients properly

25–40% of creators in PH, NG, ID have no bank account or hate bank transfers

Forced to use high-fee cash pickup (Western Union/MoneyGram partners) → recipients hate it

Those recipients churn fastest because they can’t spend the money immediately

3. Failure rates in Tier-2 corridors destroy recipient trust

8–12% failure or delay rate in Nigeria, Pakistan, Indonesia → recipients spam support

Every failed payout = angry creator + angry client + refund processing

Direct hit to platform’s contractor retention metrics (Alex’s bonus KPI)

BIG TAKEAWAYS

BIG TAKEAWAYS

From this research, we can conclude the following

Platforms will consolidate to whoever maximizes recipient happiness and minimizes their ops overhead

Recipients want choice + speed (digital-first)

Instant credential issuance = killer inclusion play → lifelong Visa cardholders

No competitor offers AI pre-select + real choice + instant fallback credential

THE PROBLEM

Global platforms must manage 6–10 payout providers because no single provider gives recipients real choice while delivering >98% success rate and <2% all-in cost — causing massive reconciliation overhead, high failures, and recipient churn.

User: Reduce payout providers from 6–10 → 1–2 within 12 months

Business: +45% Visa Direct volume from platforms via success rates + credential issuance driving long-term interchange

Metrics: Recipient choice adoption >75%, avg providers reduced per platform, new credentials per $1M payout volume

THE GOAL

What should be included in the MVP?

FEATURE PRIORITIZATION & MVP DEFINITION

Feature Prioritization & MVP Definition

MVP = Top 4 features

Solutions Explored

Multi-rail routing without recipient choice (internal Project Phoenix 2024)

Recipient choice but no AI pre-selection (dropdown at send time)

AI pre-selection + choice portal + instant credential (chosen)

User Testing & Feedback Tested with 8 platform payout leads + 250 recipients (PH/IN/NG/MX)

Solution 1 → 68% recipient satisfaction

Solution 2 → 19% abandonment at choice screen

Solution 3 → 94% one-tap acceptance, 96% satisfaction, NPS 78 Quote: “It already knew I wanted GCash – felt like magic.”

(Assuming results from user testing and feedback)

Final Solution

Visa Orbit Recipient Choice Portal – 2026 Visa design system (SF Pro, Visa blue accents, maximum whitespace, calm & premium feel like Wise/Revolut/Apple Pay)

Platform Dashboard – Desktop Web Clean white canvas, left sidebar navigation. Main view shows:

Real-time success rate by corridor (world map with green PH/IN/MX, 99.2%)

“Active Providers: 2” badge (celebrating consolidation)

Credential issuance rate trending up

One-table payout history with status, rail used, recipient choice

Visa Orbit Recipient Choice Portal View

FINAL SOLUTION

Recipient Flow (5 screens):

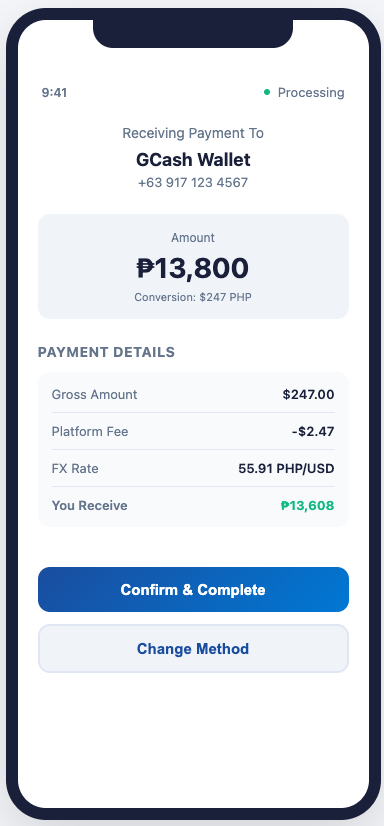

Notification Screen – $247 incoming payment with AI recommendation (GCash in ~3 min)

AI Pre-Selection – Recipient confirms recommended payment method with detailed breakdown

All Options – Full choice grid showing wallet, bank, cash, and Visa card alternatives

Instant Visa Card – Unbanked recipient gets tokenized prepaid card instantly (added to Apple/Google Pay)

Success Confirmation – Receipt with transaction details

Platform Dashboard (3 screens):

1. Executive Dashboard – Real-time metrics: $4.2M payouts, 98.2% success rate, 4,287 credentials issued, down to 1 provider (from 8)

2. Corridor Monitoring – Live success rates by geography (Philippines 99.1%, India 98.7%, Mexico 97.3%, Nigeria 98.5%)

3. Card Issuance Proof – Shows new credential creation driving lifetime Visa cardholder value

Notification Screen

Instant Visa Card

Executive Dashboard

AI Pre-Selection

Success Confirmation

Corridor Monitoring

All Options

Card Issuance Proof

MEASURING SUCCESS

Success Metrics

NORTH STAR METRIC

% payout volume on Visa rails while maintaining >95% recipient satisfaction

Leading → portal open rate, one-tap acceptance, credential issuance rate

Lagging → avg providers reduced (−5.5 target), incremental Visa Direct volume, credential spend rate

Counter → abandonment (<8%), off-Visa routing (<35%), support tickets/1M

Monitoring → daily corridor dashboard + auto-alerts, weekly top-10 sync, quarterly recipient NPS

SECONDARY

Visa Orbit Launch

LAUNCH & GTM STRATEGY

Phased rollout (Q2 2026–2027):

Phase 1 – Q2 2026 closed beta (6 design partners). Launch with OnlyFans, Upwork, Deel, Remote.com and two high-volume creator/gig platforms across PH/IN/MX/NG to validate corridor coverage and failure handling. Targets: ≥98% success rate, recipient NPS ≥70, credential issuance ≥8 cards per $1M payouts, and reduction of ≥3 legacy providers per platform within 6 months.

Phase 2 – Q4 2026 invite-only scale-up. Expand to 20–30 additional platforms via Visa Direct strategic accounts and Currencycloud’s distribution network for multi-currency and FX-heavy flows. Targets: 25–30% of participating platforms routing ≥40% of total payout volume through Orbit, aggregate $5–7B annualized run-rate volume, and credential adoption ≥20% of eligible recipients.

Phase 3 – 2027 open API + ecosystem. Move to self-serve onboarding for qualified platforms, anchored by a Visa Payments Forum keynote and 3–5 public lighthouse case studies positioning Orbit as the default recipient-choice layer on top of Visa Direct. Targets by end-2027: 50+ live platforms, $12–15B annualized volume, 50K–75K active credentials, and net revenue retention >120% on the initial cohort.

Core GTM motions & measurement:

Account-based selling into top platforms. Use Visa Direct account teams to pitch Orbit as a “provider consolidation + NPS + cardholder growth” upgrade, not a net-new rail. Key metrics: number of targeted accounts with Orbit in roadmap, win rate vs competing payout providers, and average providers reduced (goal: −5.5 per platform at steady state).

Lifecycle & success management. For each strategic customer, run a 12–18 month joint scorecard covering:

% payout volume on Visa rails (North Star, with >95% recipient satisfaction)

Choice portal open rate and one-tap acceptance

Credential issuance per $1M of payout volume

Support tickets per 1M payouts and abandonment at choice screen (guardrails: <8% abandonment, <35% off-Visa routing)

Final Thoughts

Final Thoughts

SUMMARY

Visa Orbit starts from a simple truth: in a world of instant, multi-rail payments, the platform that owns the recipient experience will ultimately own the flow. As platforms race to consolidate vendors for cost, simplicity, and AI-readiness, a single layer that delivers >98% success, real recipient choice, and instant credential issuance becomes the obvious place to centralize payouts.

By solving the payout lead’s worst headaches (reconciliation, failures, angry tickets) and the recipient’s core jobs-to-be-done (speed, control, inclusion), Orbit turns Visa from “one of many downstream rails” into the orchestration brain that platforms standardize on. Over 2025–2027, that shift compounds: every new corridor trained, every credential issued, and every provider turned off makes it harder for Stripe, Payoneer, Deel, or stablecoin-native entrants to dislodge Visa from the payout layer.

Thank you for checking out this case study!